The recent surge in the VIX (CBOE Volatility Index) at the start of the month and the proximate market correction raised a number of questions about the underlying assumptions of market behaviors in stressed environments. The rate of change of the VIX was dramatic in comparison to the record low volatility of the past year, exposing model risk that was not apparent prior to these events. This is eerily familiar to the dormant volatility period of mortgages leading up to the 2007 credit crisis and subsequent equity market route in 2008.

- Did short volatility funds cause the market sell-off, or did they simply act as catalyst that set-off a market correction that was waiting to happen?

- Did the increase in volatility cause the collapse of the short vol ETFs, or did the structure of the ETF lead to rapid vol spike and subsequent market correction?

- What model risk was exposed with the collapse of the short vol ETFs market correction?

Did short volatility funds cause the market sell-off, or did they simply act as catalyst that set-off a market correction that was waiting to happen?

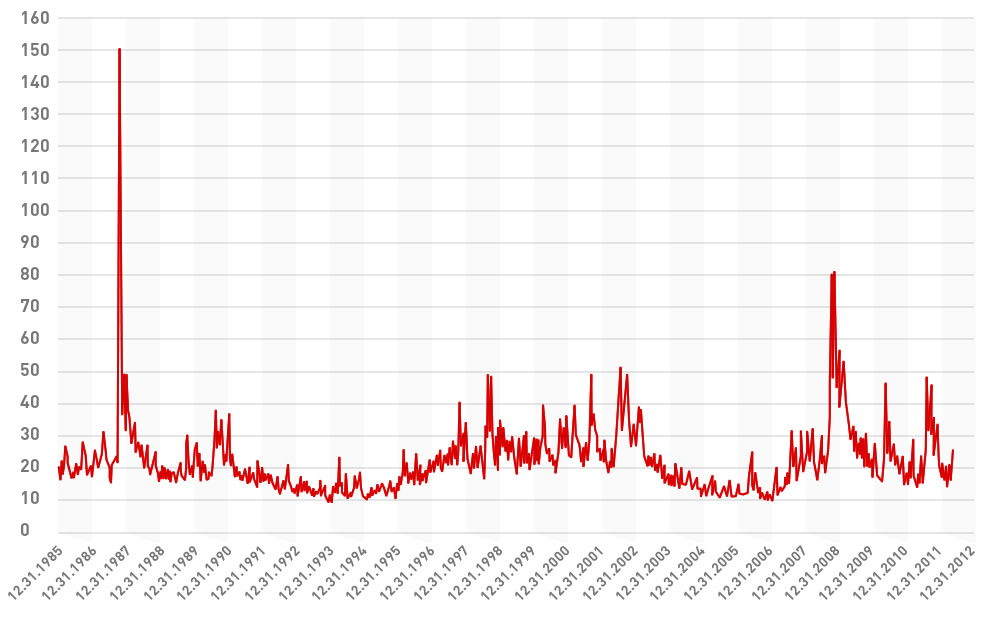

Recall that 2017 was the equivalent of pitching a perfect game. The S&P 500 gained 21.83% without a single down month or loss of more than 3% while hitting over 70 new highs. The VIX ranged from a high 17.3 to a low of 8.56 for a record low average of 11.2. After a market melt-up of 5.83% in January, market conditions deteriorated starting on January 29th with a 25% jump in the VIX and another 29% on February 2nd to reach 17.3, the highest level seen in 2017. In the same period, the S&P 500 lost 3.9%, the first drawdown of more than 3% since November 4, 2016. At the same time, we saw the 10 YR moving up from 2.66 all week then jumping on Friday after the FED released a surprise Average Hourly Earnings increase that hit the highest level since 2009, further stoking inflation fears.

CBOE Volatility Index

Annualized CBOE Volatility Index, VIX (1990 to 2017)

So that was the set-up heading into the weekend.

On Monday, February 5th, the VIX surged by 116% as the S&P 500 lost 4.1%, but the DOW witnessed a mini-flash crash of over 6% before recovering to close down 4.6%. The story gets more intriguing when we look at the XIV, the short VIX ETF, that was down only 14% at the close, but then crashed 80% after hours for a one day loss of 93% as the VIX futures continued to rise as high as 50. This exposed the structural problem with being short VIX futures and needing to rebalance each day. On February 6th, Credit Suisse announced an acceleration event had been triggered and they would redeem the fund on Feb 15. In all over $2B was lost across several short VIX ETFs. For a more detailed blow by blow see Bloomberg: Inverse-Volatility Products Almost Worked.

While there was a lot of finger pointing to the implosion of the short vol trade and how it impacted risk parity strategies, low vol funds and CTAs, this alone was not the direct cause of the ensuing market correction. However, it certainly was a catalyst for a correction that was long overdue.

Did the increase in volatility cause the collapse of the short vol ETFs or did the structure of the ETF lead to the rapid vol spike and subsequent market correction?

The success of the short vol trade ultimately became its own Frankenstein. By design, these funds were required to hedge their futures positions by the close of the market. The sheer size of these funds created a scenario whereby they would have to buy a substantial amount of the open futures if the VIX rallied, and consequently, drive the price up, thereby requiring more purchases in a vicious circle. Initially, the rise in the VIX forced the short ETFs to buy futures but it led to the futures rising because of the forced buying at the close, at which point the tail was wagging the dog. The ETFs were driving up VIX futures and no longer simply tracking it. Perhaps the fear of more shoes to drop from structured vol products motivated sellers to take profits, but this did not directly cause the losses. Three weeks after the initial vol spike of February 5th, VIX is back under 16% and the S&P 500 is only 3% below the Jan 26th high.

What model risk was exposed with the collapse of the short vol ETFs market correction?

Ample criticism of the ignorance of investors in these short vol products has been heard and for good reason. However, the behavior of the products – years of steady gains – concealed the risk of these funds. Should investors have been forewarned when the VIX jumped by 25% on the 29th and nearly 30% on February 2nd? That seems obvious now, but recall that there were three occasions in 2017 when the VIX rose by more than 30%. It was up 46.4% on May 17, 44.4% on August 10th and 32.5% on August 17th. Yet none of these led to an implosion of the funds and buying the dip in the XIV was profitable each time. So the question is, what is the tipping point? When does a VIX spike force buying that creates a vicious circle? This is where risk modeling should be very useful, but that depends on the model you choose. Given the XIV is an exchange traded product, you might easily be fooled into simply modeling it as an equity but that could be very misleading. Let’s look at the results of this type of model.

In the year prior to February 5, we see that the worst historical losses (99.9% VaR) are less than 20% for both XIV and SVXY. Even the most extreme stress scenarios only show losses of 26% to 60%.

However, the same scenarios tell a much different story after February 5th when we now see the historical loss of 82% and 92% and similar losses under a Black Monday scenario and stressing implied vols.

This is a good example of how reliant the models are on the look-back period. The risk of the short vol ETFs is simply not observed in the period leading up to the event on February 5 using this model.

After February 5th, the model is somewhat better at predicting losses except in the case of another large drop in the S&P 500 or spike in the VIX. Here we see the odd trading and mispricing behavior between February 5th and 6th when the funds suddenly plunged, a day after the VIX spike. The VIX actually settled down 20% on the 6th, the same day the short vol funds opened down dramatically and mostly stayed there. So in both cases, the market data is creating model risk that distorts possible loss scenarios.

As of February 2, 2018

| VaR Hist 99.9 | 0.1% Conditional Mean Gains – Hist | E-MINI Futures Implied Vol +100% predictive | Black Monday (1987) 1D (USD) | S&P 500 -10% Predictive | VIX +100% Predictive | |

| VIX | 25.91 | 46.38 | 328 | 254 | >165 | 100 |

| XIV | 18.01 | 12.47 | -39 | -56 | -33 | -22 |

| SVXY | 18.26 | 12.75 | -52 | -62 | -39 | -26 |

As of February 6, 2018

| VaR Hist 99.9 | 0.1% Conditional Mean Gains – Hist | E-MINI Futures Implied Vol +100% predictive | Black Monday (1987) 1D (USD) | S&P 500 -10% Predictive | VIX +100% Predictive | |

| VIX | 25.91 | 115.6 | 215 | 3,735 | 388 | 100 |

| XIV | 92.47 | 12.47 | -87 | -100 | 279 | 46 |

| SVXY | 82.96 | 12.75 | -84 | -100 | 55 | 5 |

Note: VaR is a measure of the loss

Fortunately, Red Swan Risk has perfected the tools, consultancy, and best practices that prepare our clients for the unknown.

Contact Red Swan Risk today for a demonstration of our efficient solutions for these challenges and more.

today for a demonstration